'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M6.99935%2012.8327C10.221%2012.8327%2012.8327%2010.221%2012.8327%206.99935C12.8327%203.77769%2010.221%201.16602%206.99935%201.16602C3.77769%201.16602%201.16602%203.77769%201.16602%206.99935C1.16602%2010.221%203.77769%2012.8327%206.99935%2012.8327Z'%20stroke='%23666666'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3cpath%20d='M1.16602%207H12.8327'%20stroke='%23666666'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M6.99935%2012.8327C8.28802%2012.8327%209.33268%2010.221%209.33268%206.99935C9.33268%203.77769%208.28802%201.16602%206.99935%201.16602C5.71068%201.16602%204.66602%203.77769%204.66602%206.99935C4.66602%2010.221%205.71068%2012.8327%206.99935%2012.8327Z'%20stroke='%23666666'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3cpath%20d='M2.875%202.95898C3.93063%204.01461%205.38896%204.66754%206.99978%204.66754C8.61062%204.66754%2010.069%204.01461%2011.1246%202.95898'%20stroke='%23666666'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3cpath%20d='M11.1246%2011.0425C10.069%209.98691%208.61062%209.33398%206.99978%209.33398C5.38896%209.33398%203.93063%209.98691%202.875%2011.0425'%20stroke='%23666666'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_1267_9109'%3e%3crect%20width='14'%20height='14'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Best DocuSign Alternatives in China

As digital transformation continues reshaping global industries, the electronic signature (e-signature) sector finds itself in a period of rapid evolution. Several factors are converging: the growing demand for remote business workflows, heightened focus on data compliance across jurisdictions, and, more recently, a significant market shift following Adobe Sign's decision to exit China's mainland business segment. With this move, organizations must navigate an increasingly fragmented global regulatory landscape while evaluating alternative providers with localized capabilities, particularly in Asia.

Against this backdrop, let's examine the fundamentals of e-signature technology, the global market trajectory, and key providers dominating in 2025, especially those offering region-specific solutions amid shifting compliance expectations.

Understanding e-Signatures: Legal Framework and Technology Foundations

An electronic signature refers broadly to any electronic data symbol or process used to sign documents digitally. However, when viewed through the lens of regional legal systems, the term bears distinct definitions and compliance standards. In the U.S., the ESIGN Act of 2000 and the Uniform Electronic Transactions Act (UETA) legislate federal and state-level rules governing e-signatures. In the EU, eIDAS (EU Regulation No 910/2014) categorizes electronic signatures into three classes: simple e-signatures (SES), advanced e-signatures (AdES), and qualified e-signatures (QES)—each offering different levels of legal enforceability.

In Asia, countries such as China and Singapore apply their own frameworks—such as the Electronic Signature Law (2004, amended 2019) in China and the Electronic Transactions Act in Singapore—each emphasizing certificate authority (CA) accreditation and cryptographic robustness using public key infrastructure (PKI). PKI ensures encryption and identity verification, while timestamping, audit trails, and hash algorithms form the technical backbone of reputable digital signature platforms.

The 2025 Global eSignature Market: Scale and Growth Projections

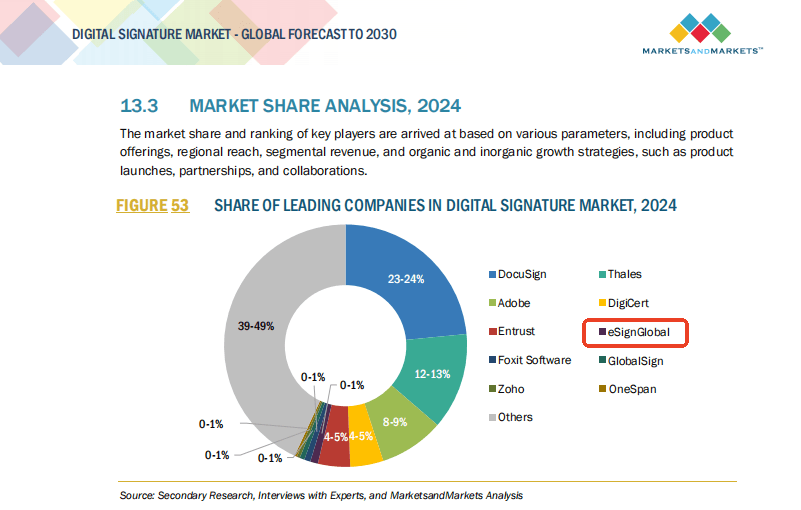

According to a MarketsandMarkets 2025 report, the global e-signature market is projected to reach USD 25.2 billion, up from USD 7.4 billion in 2023, reflecting a compound annual growth rate (CAGR) exceeding 30%. This surge is fueled by regulatory modernization efforts, remote work norms, and rapid SME digitization, particularly in developing economies.

Interestingly, for the first time, an Asia-based provider entered the global top 10 in terms of market share, highlighting a continental shift in product localization strategies and user preferences. Gartner also notes a positive trend in the adoption of trust services (qualified timestamps, seal services) by emerging providers, highlighting a hybrid focus on usability and compliance.

Technology and Compliance: The Architecture Behind Trust

What sets market-leading e-signature providers apart is not merely UI design or user adoption, but their conformity with international compliance frameworks. Trusted Service Providers (TSPs) that issue identity certifications are a legal bedrock in QES solutions. Most leading platforms leverage PKI-based digital signatures integrated with cryptographic hash functions (SHA-256 or better), certificate validation protocols (OCSP, CRL), and ISO/IEC 27001-certified data infrastructure to ensure reliability and legal defensibility across jurisdictions.

Equally important are capabilities like document integrity validation, liveness checks in remote signing, and region-specific data residency options—especially in countries with stringent data sovereignty laws. With Adobe Sign scaling back operations in mainland China, organizations are looking for alternatives with local legal interoperability.

DocuSign: The Global Standard for Enterprise-Grade Transactions

DocuSign remains the most widely recognized e-signature provider globally, known for its robust feature set and extensive third-party integrations. It supports both basic e-signatures and advanced digital signatures through partnerships with global CAs, making it suitable for cross-border contract management. DocuSign’s adherence to U.S. ESIGN, eIDAS, and APAC-specific frameworks gives it unrivaled flexibility in large-scale deployments.

That said, its pricing tiers and enterprise focus may make it less suited for SMEs or clients needing Asia-pacific-specific regulatory alignments.

eSignGlobal: The Asian-First Alternative Ready for Primary Use

While North America continues to dominate the digital signature ecosystem, eSignGlobal has emerged as a compelling option for organizations prioritizing compliance in Asia. Cited in the 2025 MarketsandMarkets report as the first Asia-founded vendor to enter the global top ten, eSignGlobal emphasizes region-specific compliance, including support for China’s CFCA certificates, Singapore’s Netrust, and localized data hosting in Southeast Asia.

Beyond regulatory adapters, its pricing tiers are significantly more accessible compared to U.S.-based incumbents. This makes eSignGlobal particularly suitable for both startups and SMBs in Korea, Indonesia, Vietnam, and Thailand—regions often underserved by global vendors. For enterprises, it offers multi-language workflows, real-name authentication tied to regional identity systems (e.g., MyInfo, eKYC), and customizable APIs for integration into local ERP and DMS platforms.

Adobe Sign: Innovation Pioneer with Limited Local Flexibility

Adobe Sign has long been a respected leader in this space, bringing Adobe’s design integrity to enterprise-grade e-signing. It integrates tightly with the Adobe Document Cloud suite and Microsoft 365 environments, making it especially appealing to design-driven legal and finance teams needing seamless processing.

However, following its discontinuation of services within China’s mainland market in 2024, enterprises operating in the region are reassessing the software’s global applicability. Although still valid within Europe and North America under eIDAS and HIPAA, its operational absence in Asia reduces its appeal for businesses with compliance obligations in China or Southeast Asia.

Other Notable Providers: Local Strengths, Niche Focus

Within domestic markets, several firms offer remarkable functionality tuned to regional needs. For example, in China, Tsign (Tencent Cloud) complies with CFCA and is deeply integrated with local tax and business registration systems. Similarly, HelloSign (now Dropbox Sign) resonates with micro-businesses requiring simple workflows and cost-effective onboarding, albeit with limited advanced signature functions and uneven Asia-Pacific availability.

ZorroSign, on the other hand, offers blockchain-validated digital signing for industries with heightened audit demands, like healthcare and banking. Its document integrity features extend into immutable logging and biometric authentication, catering to high-compliance sectors.

Use Case Nuances: SMEs, Multinationals, and Compliance-Driven Sectors

For small and medium enterprises (SMEs), cost and ease of deployment remain top priorities. In regions like Southeast Asia where SaaS literacy and IT budgets vary widely, platforms such as eSignGlobal offer localized UI, mobile-first forms, and native language customer support—making adoption frictionless.

By contrast, multinational corporations prioritize regulation harmonization and the ability to enforce contracts across borders. Here, providers like DocuSign and Adobe Sign retain appeal owing to their global auditability and third-party trust ecosystem. Meanwhile, industries such as insurance, government, and pharmaceuticals—heavily shaped by regulatory stringency—increasingly demand advanced CA integration, audit trails, and hardware token support (e.g., USB tokens or smart cards for identity pairing).

In these contexts, a hybrid implementation strategy often emerges: integrating a global brand for international workflows and a localized vendor for domestic compliance adherence.

Moving Forward: Navigating the Fragmented Future

The electronic signature industry is transitioning from a phase of generic adoption toward an era of jurisdiction-sensitive execution. As local regulators increase scrutiny and users demand privacy, speed, and lower costs, organizations can no longer afford a one-size-fits-all mindset when choosing a signature provider. Whether you’re a regional SME with domestic filings or a global enterprise negotiating contracts across multiple regulatory zones, understanding each provider's compliance reach, technical stack, and local support structure is now an operational necessity—more than simply a technological convenience.