'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M6.99935%2012.8327C10.221%2012.8327%2012.8327%2010.221%2012.8327%206.99935C12.8327%203.77769%2010.221%201.16602%206.99935%201.16602C3.77769%201.16602%201.16602%203.77769%201.16602%206.99935C1.16602%2010.221%203.77769%2012.8327%206.99935%2012.8327Z'%20stroke='%23666666'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3cpath%20d='M1.16602%207H12.8327'%20stroke='%23666666'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M6.99935%2012.8327C8.28802%2012.8327%209.33268%2010.221%209.33268%206.99935C9.33268%203.77769%208.28802%201.16602%206.99935%201.16602C5.71068%201.16602%204.66602%203.77769%204.66602%206.99935C4.66602%2010.221%205.71068%2012.8327%206.99935%2012.8327Z'%20stroke='%23666666'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3cpath%20d='M2.875%202.95898C3.93063%204.01461%205.38896%204.66754%206.99978%204.66754C8.61062%204.66754%2010.069%204.01461%2011.1246%202.95898'%20stroke='%23666666'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3cpath%20d='M11.1246%2011.0425C10.069%209.98691%208.61062%209.33398%206.99978%209.33398C5.38896%209.33398%203.93063%209.98691%202.875%2011.0425'%20stroke='%23666666'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_1267_9109'%3e%3crect%20width='14'%20height='14'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

How to use e-signatures in financial services while remaining compliant?

The Rise of E-Signatures in Financial Services

In the fast-paced world of financial services, electronic signatures (e-signatures) have become indispensable tools for streamlining operations, from loan approvals to contract executions. They offer efficiency, reducing paperwork and turnaround times while enabling remote transactions. However, ensuring compliance with stringent regulations is paramount to avoid legal pitfalls and maintain trust. This article explores practical strategies for integrating e-signatures into financial workflows while prioritizing regulatory adherence, drawing on industry observations.

Understanding Key Compliance Requirements for E-Signatures in Finance

Financial institutions operate under a web of regulations designed to protect sensitive data and ensure transaction integrity. In the United States, the Electronic Signatures in Global and National Commerce Act (ESIGN Act) and the Uniform Electronic Transactions Act (UETA) provide the legal foundation for e-signatures, treating them as equivalent to wet-ink signatures if certain conditions are met. These include demonstrating intent to sign, consent to electronic records, and the ability to retain records in a form that can be accurately reproduced.

For international operations, compliance extends to frameworks like the EU's eIDAS Regulation, which categorizes e-signatures into simple, advanced, and qualified levels, with qualified electronic signatures (QES) offering the highest legal certainty—essential for cross-border financial deals. In Asia-Pacific (APAC) regions, such as China and Singapore, local laws like the Electronic Signature Law of the People's Republic of China mandate specific authentication methods, including real-name verification and timestamping.

Beyond legal validity, financial services must address anti-money laundering (AML) and know-your-customer (KYC) requirements under laws like the Bank Secrecy Act (BSA) in the US or the Financial Action Task Force (FATF) recommendations globally. E-signatures must integrate robust identity verification to prevent fraud, such as biometric checks or multi-factor authentication (MFA). Data privacy is another cornerstone; regulations like the General Data Protection Regulation (GDPR) in Europe and the California Consumer Privacy Act (CCPA) demand secure storage, encryption, and user consent for data processing.

From a business perspective, non-compliance can lead to hefty fines—up to 4% of global revenue under GDPR—or reputational damage. Institutions should conduct regular audits to verify that e-signature platforms log all actions immutably, providing tamper-evident audit trails that detail signer identity, timestamp, and IP address.

Implementing E-Signatures Compliantly: Step-by-Step Guide

To harness e-signatures effectively in financial services without compromising compliance, follow these structured steps, informed by best practices observed in the sector.

Step 1: Select a Compliant E-Signature Platform

Choose providers certified under relevant standards, such as ISO 27001 for information security or SOC 2 for trust services. For financial use cases, prioritize platforms supporting advanced features like qualified electronic signatures for high-stakes documents (e.g., mortgages or investment agreements). Evaluate integration with existing systems like CRM or core banking software to ensure seamless workflows.

In practice, financial firms should request vendor compliance reports and third-party audits. For instance, when handling client onboarding, the platform must support KYC-compliant identity proofing, such as government ID verification or knowledge-based authentication.

Step 2: Establish Robust Identity Verification Processes

Identity assurance is non-negotiable in finance. Implement multi-layered verification: start with email or SMS OTP for low-risk documents, escalating to biometrics or video KYC for high-value transactions. Platforms should allow conditional routing, where signers provide attachments like passports only if required by jurisdiction.

Business observers note that integrating e-signatures with AML screening tools can automate red-flag detection, reducing manual reviews by up to 50%. Always obtain explicit consent for electronic signing, documenting it to satisfy ESIGN Act requirements.

Step 3: Ensure Secure Document Handling and Storage

Use end-to-end encryption (AES-256 standard) for documents in transit and at rest. Platforms must offer role-based access controls, preventing unauthorized views. For long-term retention—often mandated for 7+ years in finance—opt for cloud storage compliant with data residency laws, avoiding cross-border transfers that could trigger GDPR scrutiny.

Audit trails are critical: every e-signature event should generate a verifiable log, exportable for regulatory inquiries. In observed cases, firms using such systems have successfully defended against disputes by providing immutable proof of execution.

Step 4: Train Staff and Monitor Ongoing Compliance

Compliance isn't a one-time setup; it requires ongoing education. Train teams on platform use, emphasizing red flags like unusual signer behavior. Implement automated alerts for expiring consents or incomplete verifications.

Regularly review platform updates for new regulations, such as evolving APAC digital identity standards. Partner with legal experts to map workflows against jurisdiction-specific rules, ensuring scalability as operations expand.

Step 5: Test and Audit Workflows

Pilot e-signature integrations with sample financial documents, simulating real scenarios like wire transfer authorizations. Conduct penetration testing to identify vulnerabilities. Post-implementation, perform quarterly audits, leveraging platform analytics to track compliance metrics like verification success rates.

By following these steps, financial services can achieve 80-90% faster processing times while mitigating risks, as evidenced by industry benchmarks from firms like banks adopting e-signatures during digital transformations.

Challenges with Established E-Signature Providers in Financial Contexts

While e-signatures offer clear benefits, selecting the right provider is tricky due to varying compliance support and operational hurdles, particularly for global financial operations.

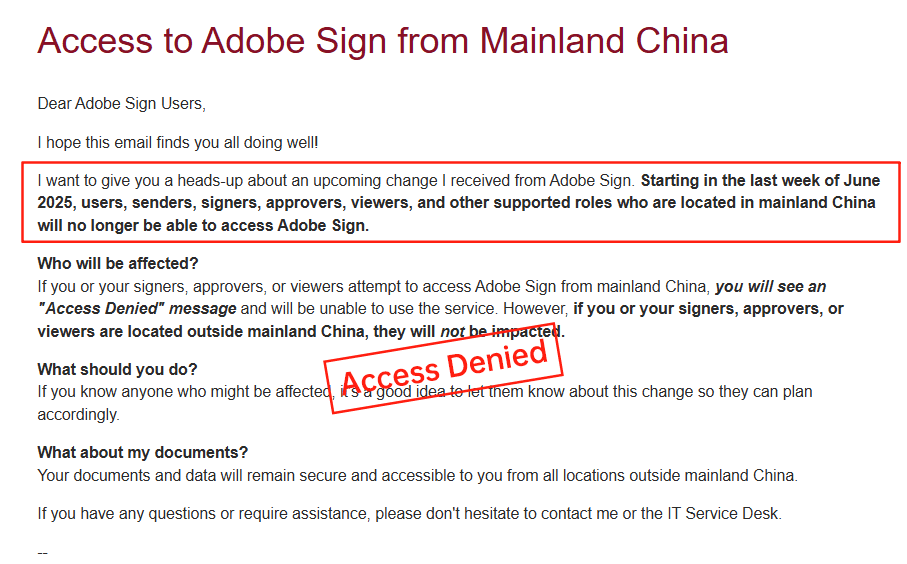

Adobe Sign: Transparency and Market Withdrawal Issues

Adobe Sign has been a staple for document management, but its pricing lacks transparency, often bundling e-signature features within broader Adobe ecosystem subscriptions without clear breakdowns for usage-based fees. This opacity can lead to unexpected costs for high-volume financial workflows. More critically, Adobe Sign announced its withdrawal from the Chinese mainland market in 2023, citing regulatory complexities, which disrupts APAC-focused financial institutions reliant on seamless regional operations. This exit forces users to seek alternatives for China-compliant signing, complicating multi-jurisdictional compliance.

DocuSign: High Costs and Regional Service Gaps

DocuSign dominates the e-signature space with robust features, but its pricing structure—starting at $10/month for basic plans and scaling to custom enterprise tiers—can be prohibitively expensive, especially with add-ons like identity verification or API usage. Annual plans for business features reach $480/user, yet envelope limits (around 100/year) and metered fees for automation sends create unpredictability. Transparency issues arise from non-public enterprise pricing and region-dependent surcharges.

In long-tail regions like APAC, DocuSign faces challenges: cross-border latency slows document loading, limited local ID methods hinder compliance, and higher support costs inflate totals. For financial services in China or Southeast Asia, these factors can undermine efficiency, prompting observations of inconsistent service quality compared to region-optimized tools.

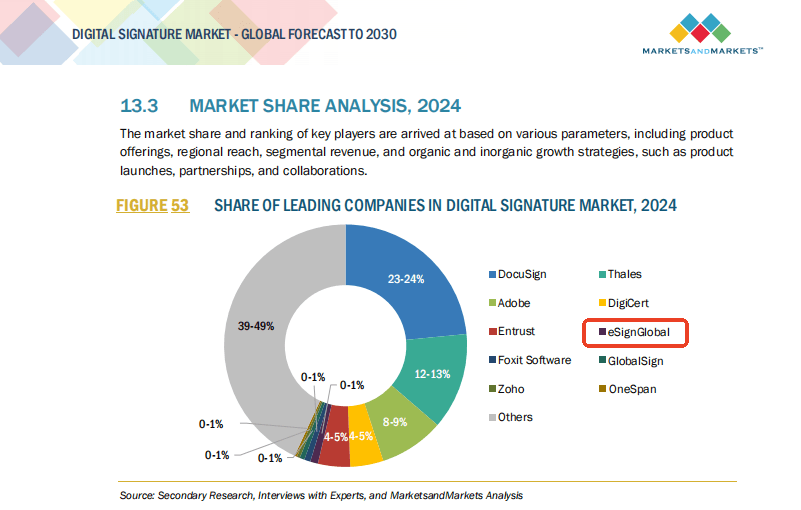

eSignGlobal: A Regionally Tailored Alternative

eSignGlobal emerges as a viable option, particularly for APAC-centric financial operations, offering transparent pricing and native compliance with local laws like China's Electronic Signature Law. It supports fast, low-latency signing optimized for cross-border deals, with flexible API costs and regional data residency options. Features like integrated KYC and biometric verification align well with financial needs, providing a balanced alternative without the premium pricing pitfalls of larger providers.

Comparing E-Signature Providers for Financial Compliance

To aid decision-making, here's a neutral comparison of key providers based on financial services criteria:

| Aspect | DocuSign | Adobe Sign | eSignGlobal |

|---|---|---|---|

| Pricing Transparency | Moderate; usage-based add-ons unclear | Low; bundled in ecosystem, hard to isolate | High; flexible, region-specific plans |

| APAC/China Compliance | Partial; latency and limited local support | Withdrawn from China market | Strong; native alignment with CN/SEA laws |

| Cost for Financial Use | High ($300–$480/user/year + extras) | Variable, often enterprise-tied | Competitive; optimized for regional volume |

| Identity Verification | Metered, advanced options available | Basic to advanced, but regional gaps | Integrated KYC/biometrics, cost-effective |

| Speed in Long-Tail Regions | Inconsistent due to global infrastructure | N/A post-withdrawal in key areas | Optimized for APAC, low latency |

| Overall Suitability for Finance | Robust for US/EU, but costly for global | Good for Adobe users, limited reach | Ideal for cross-border APAC finance |

This table highlights trade-offs, with eSignGlobal standing out for regional efficiency without sacrificing core compliance.

Final Thoughts: Choosing the Right Path Forward

Navigating e-signatures in financial services demands a balance of innovation and caution. For institutions seeking DocuSign alternatives with strong regional compliance—especially in APAC—eSignGlobal offers a practical, compliant choice tailored to global financial demands. Evaluate based on your specific needs to ensure sustained operational success.

FAQs