'%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M6.99935%2012.8327C10.221%2012.8327%2012.8327%2010.221%2012.8327%206.99935C12.8327%203.77769%2010.221%201.16602%206.99935%201.16602C3.77769%201.16602%201.16602%203.77769%201.16602%206.99935C1.16602%2010.221%203.77769%2012.8327%206.99935%2012.8327Z'%20stroke='%23666666'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3cpath%20d='M1.16602%207H12.8327'%20stroke='%23666666'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M6.99935%2012.8327C8.28802%2012.8327%209.33268%2010.221%209.33268%206.99935C9.33268%203.77769%208.28802%201.16602%206.99935%201.16602C5.71068%201.16602%204.66602%203.77769%204.66602%206.99935C4.66602%2010.221%205.71068%2012.8327%206.99935%2012.8327Z'%20stroke='%23666666'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3cpath%20d='M2.875%202.95898C3.93063%204.01461%205.38896%204.66754%206.99978%204.66754C8.61062%204.66754%2010.069%204.01461%2011.1246%202.95898'%20stroke='%23666666'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3cpath%20d='M11.1246%2011.0425C10.069%209.98691%208.61062%209.33398%206.99978%209.33398C5.38896%209.33398%203.93063%209.98691%202.875%2011.0425'%20stroke='%23666666'%20stroke-linecap='round'%20stroke-linejoin='round'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_1267_9109'%3e%3crect%20width='14'%20height='14'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

China’s E-Signature Ecosystem: Regulation, Technology, and Global Expansion

In recent years, as digital transformation accelerates, enterprises and governments have placed greater emphasis on security, compliance, and efficiency. Digital signatures, as a critical technology for ensuring document integrity and identity authentication, are experiencing rapid growth. According to the report Digital Signature Market – Global Forecast to 2030, the global digital signature market was valued at USD 5.2 billion in 2022 and is expected to reach USD 35.4 billion by 2030, with a compound annual growth rate (CAGR) of 27.1% between 2023 and 2030. This strong growth underscores the global shift from traditional paper-based signing to digital signing, spanning industries such as government, finance, healthcare, and legal services.

Steady Global Expansion, with Asia-Pacific Leading Growth

The report highlights that North America held the largest market share in 2022, driven by the U.S. and Canada’s strong emphasis on digital identity, mature regulatory frameworks, and early enterprise adoption. Laws such as the ESIGN Act and UETA provide a legal foundation for digital signatures, accelerating adoption in finance, government, and enterprise services.

While North America currently leads, Asia-Pacific is projected to be the fastest-growing market during 2023–2030. Countries such as China, Japan, India, and Southeast Asian economies are driving demand through digital governance, fintech adoption, and remote-work infrastructure. For example, China’s revisions to its Electronic Signature Law in recent years have created new growth opportunities for domestic providers.

Solution Types: Software Dominates, Services Accelerating

The market is broadly segmented into two solution categories: software and services. As of 2022, software solutions accounted for the largest share, due to enterprises’ and governments’ demand for secure, sustainable signing systems. Software solutions are cost-efficient post-deployment and can be integrated seamlessly into existing systems via APIs or SDKs. In sectors such as finance and healthcare, demand for automated, high-volume, and compliance-focused solutions is particularly strong.

However, the services segment is expected to grow at a faster pace. Managed signing, signature-as-a-service (SaaS), and consulting on signing workflows are becoming key to improving efficiency and lowering IT entry barriers. Many SMEs, driven by cost and resource constraints, prefer ready-to-use signing services, fueling rapid growth in the services market.

Deployment Models: Cloud as the Preferred Architecture

Deployment modes are shifting decisively toward cloud-based solutions. While on-premises deployment still serves industries with stringent policy requirements—such as government and defense—cloud solutions have become mainstream due to scalability, high availability, and ease of integration.

By 2030, cloud deployments are expected to dominate the market. SaaS models allow providers to deliver on-demand digital signing services through subscription, reducing installation and maintenance burdens while supporting flexible remote work needs. Leading digital signature vendors are expanding their cloud capabilities to address the surging demand across regions and industries.

Industry Adoption: BFSI and Government Lead Demand

By verticals, BFSI (banking, financial services, and insurance) represented the largest share in 2022. High transaction volumes, broad customer bases, and strict regulatory requirements drive strong reliance on enterprise-grade digital signature solutions.

Government agencies are the second-largest adopters, as e-government initiatives accelerate and regulations on digital document management mature. Increasingly, governments deploy digital signatures for document processing, approvals, and identity authentication—particularly in Asia-Pacific and parts of Europe.

The report also highlights the growing adoption among SMEs. With limited IT resources, SMEs increasingly choose SaaS-based digital signature platforms to balance cost-efficiency with compliance.

Regional Analysis: North America Steady, Asia-Pacific Rising

In 2022, North America maintained its lead, with the U.S. driving adoption across finance, legal, and healthcare sectors. Market leaders have built strong sales and support networks in the region, ensuring a stable market base.

Asia-Pacific, however, shows stronger growth momentum. Population advantages, mobile penetration, and government-led digital governance initiatives are fueling demand. In markets like China and India, large-scale e-government projects are accelerating the upgrade of digital signing infrastructure.

Technology Trends: PKI at the Core, Integration and Scalability in Focus

Public Key Infrastructure (PKI) remains the foundation of digital signature technology, ensuring authenticity, non-repudiation, and data integrity. As compliance and audit requirements intensify, demand for advanced recordkeeping and audit trail functions is driving new product development.

Integration capabilities are also emerging as a key differentiator. Enterprises increasingly require platforms that support APIs, secure interfaces, and seamless collaboration with ERP and other enterprise systems. Vendors focusing on workflow automation and cross-platform interoperability are expected to gain a competitive edge.

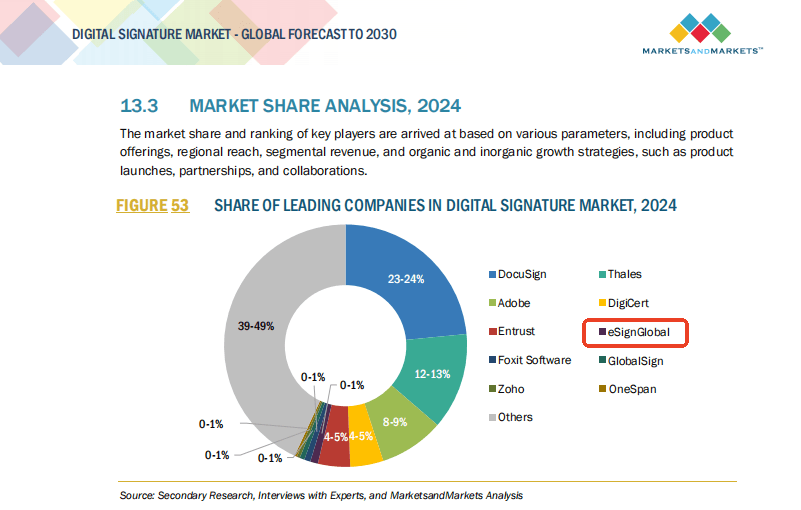

Leading Enterprises: eSign and eSignGlobal

The report highlights several key players with leadership positions. Among them are China’s eSign and the international platform eSignGlobal.

eSign: As China’s leading digital signature platform, eSign has built a strong track record across government, finance, and legal sectors. Its deep alignment with local compliance requirements and robust technology stack have established a solid competitive moat. Beyond large enterprises, eSign is rapidly expanding into SME and consumer markets.

eSignGlobal: Positioned as a global service provider, eSignGlobal focuses on cross-border document workflows, multilingual interfaces, and blockchain-backed transparency. Its solutions are trusted in financial services, international trade, and legal documentation, making it a strong player in both Western and Asia-Pacific markets.

Outlook to 2030: Compliance-Driven, Technology-Powered Growth

According to the Digital Signature Market – Global Forecast to 2030, digital signatures are moving from early adoption to full-scale commercialization, underpinned by regulatory mandates and technological advancements. Legal frameworks, refined industry requirements, integrated technologies, and cloud deployment together form the foundation for sustained market expansion.

Across solutions, industries, and geographies, the digital signature market is increasingly characterized as a core component of the modern information economy. Providers like eSign and eSignGlobal—combining platform strength, technical capabilities, and localized services—are well positioned to lead the market toward compliance, security, and efficiency.

As global trust in digital ecosystems deepens, digital signatures will become indispensable infrastructure for digital governance and international trade.